Executive pension plans, 1e pension plans & co.: optimizing pension solution models

Why it is worth separating your extra-mandatory provisions

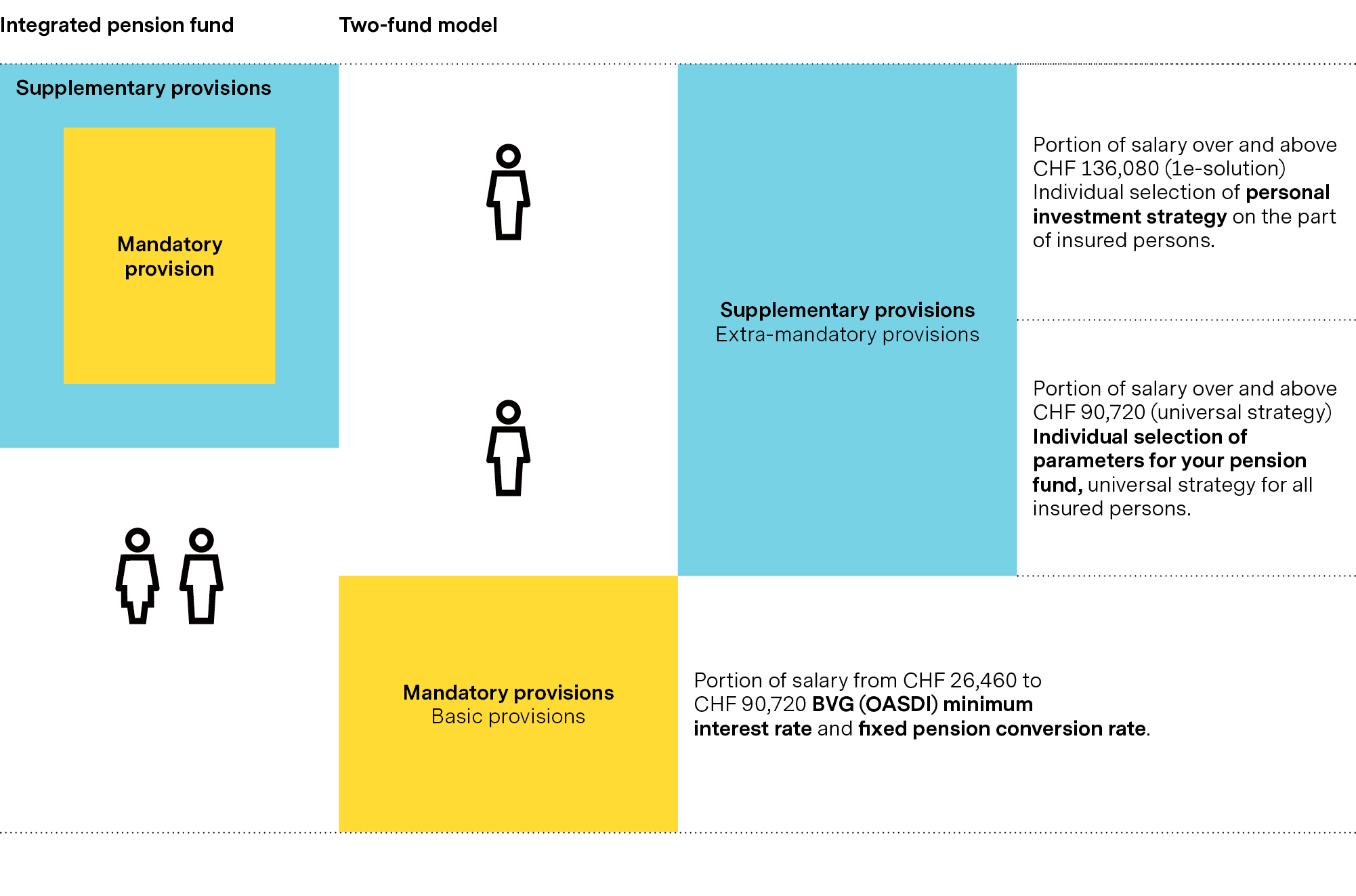

A pension fund with an integrated model does not address the needs of the insured persons; rather, it must fulfil its high levels of obligations in the short term. I.e., promised provision comes into conflict with minimum interest and conversion rates. An inflated conversion rate for mandatory provisions tends to lead to integrated pension funds setting exaggeratedly low conversion rates on extra-mandatory provisions, which encourages cross-subsidization.

Thus, more and more often, mandatory and extra-mandatory provisions are separated from one another and invested into two different solutions. This offers the opportunity of optimizing the individual solutions to better suit personal needs. It also reduces cross-subsidization as far as is possible.

Source: Vontobel. An executive pension plan offers the possibility of achieving more individual provisions goals.

An example of the advantages of an extra-mandatory pension plan

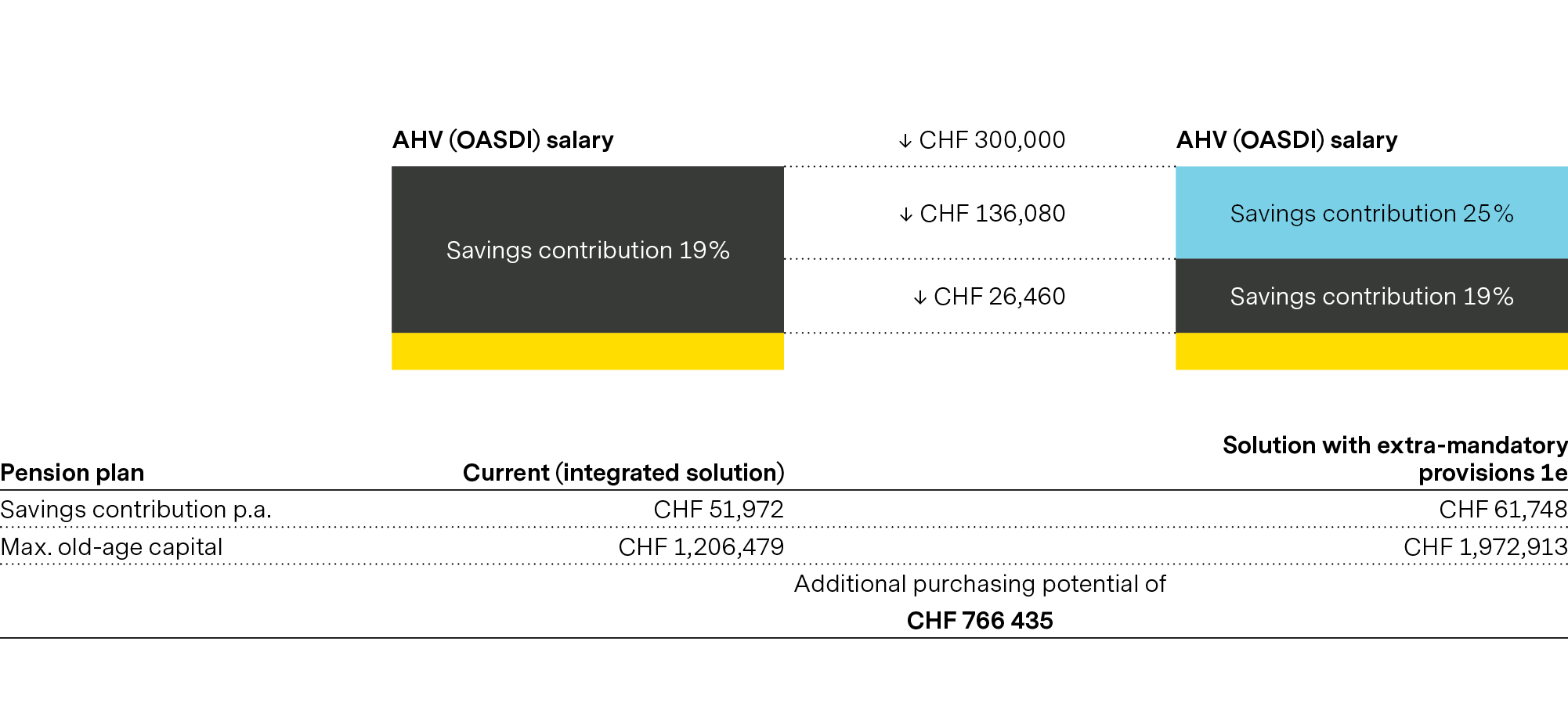

In a so-called 1e pension plan, the annual savings premium may amount to max. 25 percent of the insured annual salary, whereby a maximum salary of CHF 907,200 can be taken into consideration. A company may offer up to three pension plans, with differing levels of savings contributions, for each employee category. This means that insured persons may decide for themselves whether they pay e.g., 15, 20 or 25 percent of their insured salary into the plan. Employer contributions must be the same for all three plans.

The following example shows optimization potential:

A self-employed solicitor, 55-years old, OADI salary CHF 300,000

Source: Vontobel. In this case, an executive plan is useful: Higher annual savings contributions and higher voluntary buying-in.

A 55-yearold solicitor earns CHF 300,000 per annum. The current pension plan insures the coordinated annual salary, the savings share amounts to 19 percent. The share of the salary between CHF 26,460 (coordination deduction) and CHF 136,080 is insured as in the past. New: On the share of the salary over and above CHF 136,080 the savings premium is raised to the legal maximum of 25 percent. Thereby the solicitor’s annual savings contribution goes up from CHF 51,972 to CHF 61,748 per annum. The additional savings premium reduces taxable income and expanded pension provisions increase potential for voluntary buying-in. The solicitor may now pay around CHF 766,000 more than previously into the second pillar and may deduct that amount from taxable income over a period of several years.

The second major advantage: Individual investment strategy

In addition to customized pension plans, 1e pension plans also allow all insured persons to pursue individual investment strategies. Insured persons of any pension fund are different with regard to risk capacity and propensity. In an integrated pension fund solution, the principle is “One size fits all.” All insured persons are in the same “pot” and must allow their capital to be invested according to a standardized strategy. In contrast, with an extra-mandatory plan, they benefit from a range of investment strategies and can flexibly tailor coverage to their personal needs and to the current capital market situation.

Overview: Why an extra-mandatory solution is often the right one

Pension funds need to adapt their respective investment strategies according to their structural risk capacity. For that reason, as a rule, they can only invest moderately in equities. In addition, insured persons only benefit in part from the returns which are generated because these are used for technical adjustments and for building value fluctuation reserves. Against this background, an individual investment strategy which is tailored to your own risk capacity makes sense and makes 1e extra-mandatory solutions even more attractive.

It would enable you to largely eliminate demographic challenges and the above-mentioned problem of cross-subsidization. Generally speaking, modern solutions in the field of occupational pension provisions coordinate retirement capital with free assets to achieve an advantageous overall asset allocation.

Systematic and long-term planning

Over and above a certain level of income, you could save a considerable amount of retirement capital if you plan your extra-mandatory coverage systematically and for the long term – and save on tax at the same time. You also benefit from an individual investment strategy. In addition, later on, when you start drawing your retirement capital, there are various further optimization possibilities.

It is worth tackling your future provisions early on. Our specialists would be pleased to help you find the best solutions for preparing for your retirement. Contact us for an initial discussion, without any obligation.

Updated on 01.06.2025 CEST

Published on 11.03.2024 CET

ABOUT THE AUTHORS

Show more articles

Show more articlesAlexander Spillmann

Head Pension Solutions