5 investment myths debunked

Myth 1: Cash is safe

Myth 1: Cash is safe

In fact, hoarding cash leads to devaluation by inflation. Your money buys a lot less.

Source: Vontobel 2022.

Myth 2: You need to wait for the right moment to enter

Actually, compound interest effects can tip the balance of your investmentSource: Vontobel 2022; for illustrative purposes only.

Four ways of investing 100 USD over twenty years: Investors who enter the market at once unlock better long-term compound effects compared to investors who stagger the same amount over time. Illustration based on an estimated 10% returns per annum.

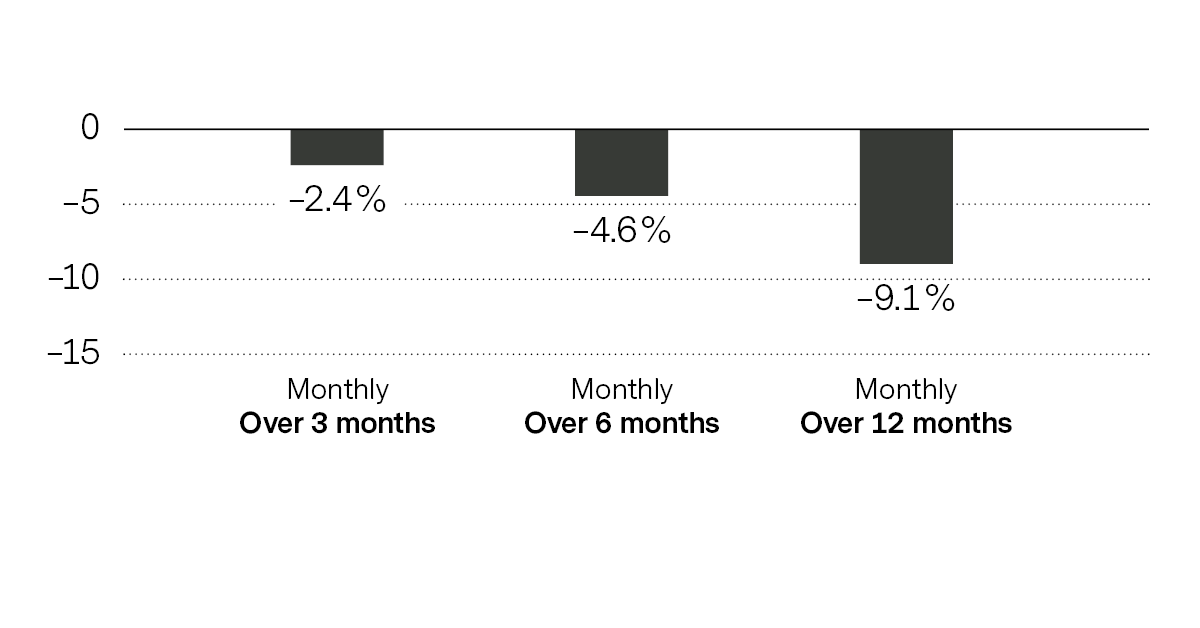

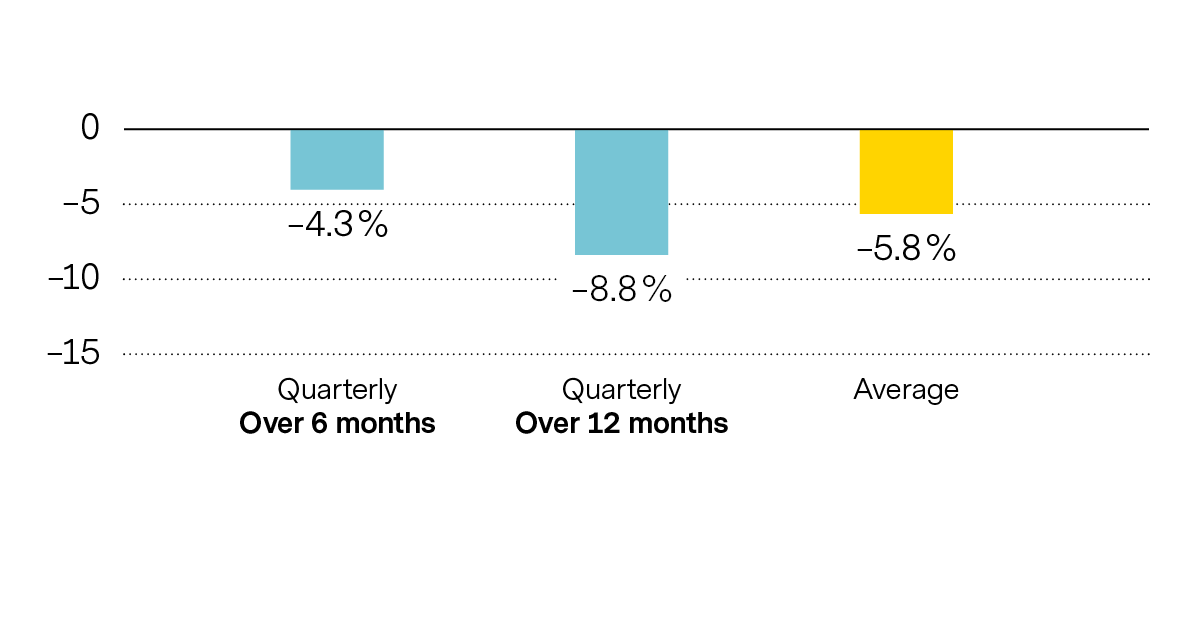

Myth 3: Timing the market is the only source of returns

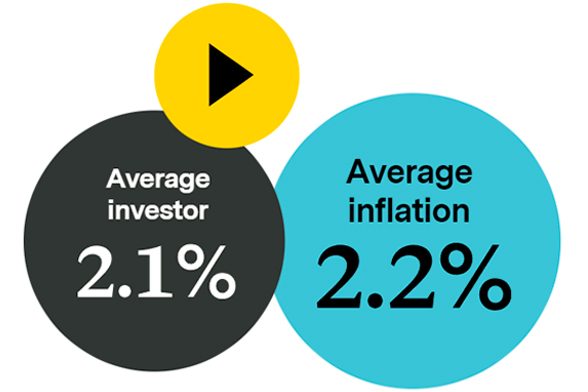

What does history teach investors?

The average investor does not retain real wealth.

Source: Inflation based on US Consumer Price Index (CPI); average investor represented by Dalbar’s average asset allocation investor return, which utilizes the net of average mutual fund sales, redemptions and exchanges each month (“Investing & Emotions”, BlackRock Investment Insight 2016).

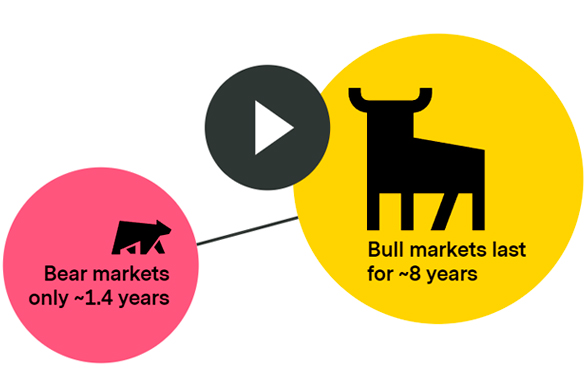

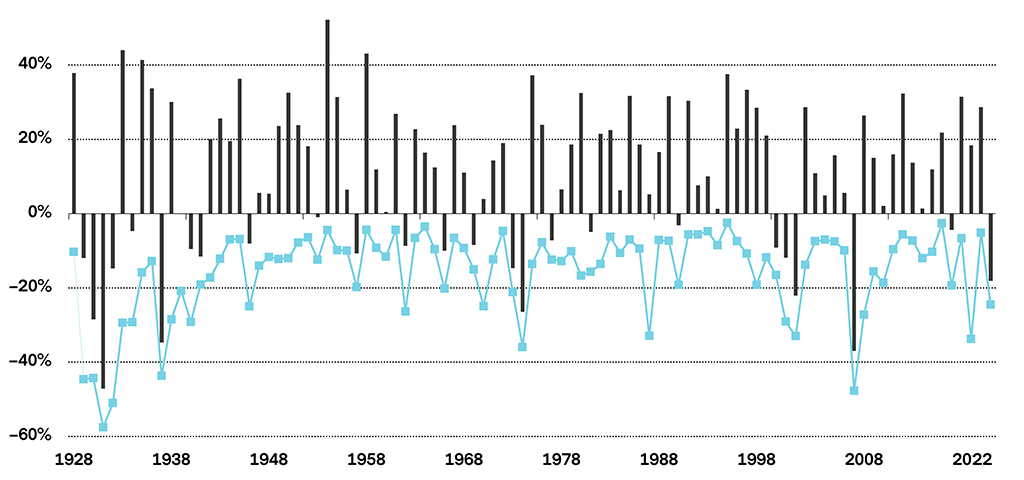

Don’t be afraid—bulls have endurance, bears don’t

Source: Vontobel 2022.

In the bear market, it’s the perspective that matters

Despite investor’s natural bias to vividly remember bear days, only a small number of trading periods were actually bearish in the past. Chart compares the number of bear market days versus the number of bull market days per occurrence, summed up as average of years.

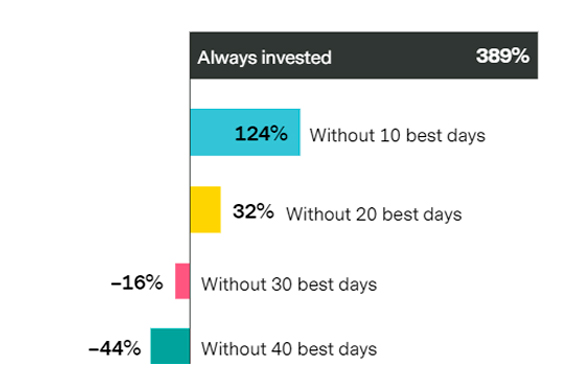

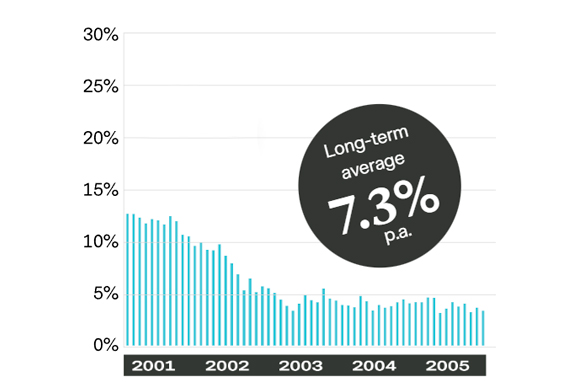

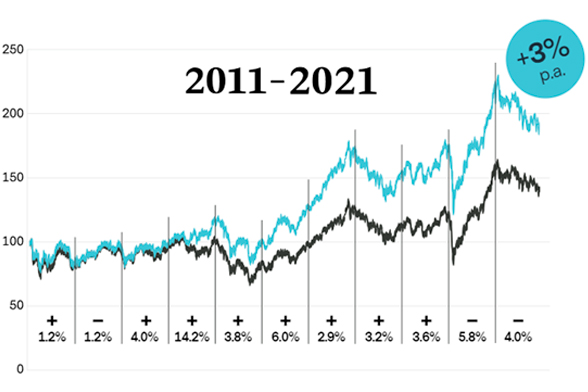

Time in the market is the long-term investor’s business

A look at the total returns in global equities between 1999 and 2022, demonstrates where the “fear of missing out” (FOMO) comes from—and that staying invested can be your antidote.

Source: Bloomberg, based on the index MSCI ACWI from 01.01.1999 to 31.12.2022, daily total returns (including dividends), gross.

Note: Past performance is not a reliable indicator of current or future performance.

Myth 4: Portfolio diversification is good for safety, not for returns

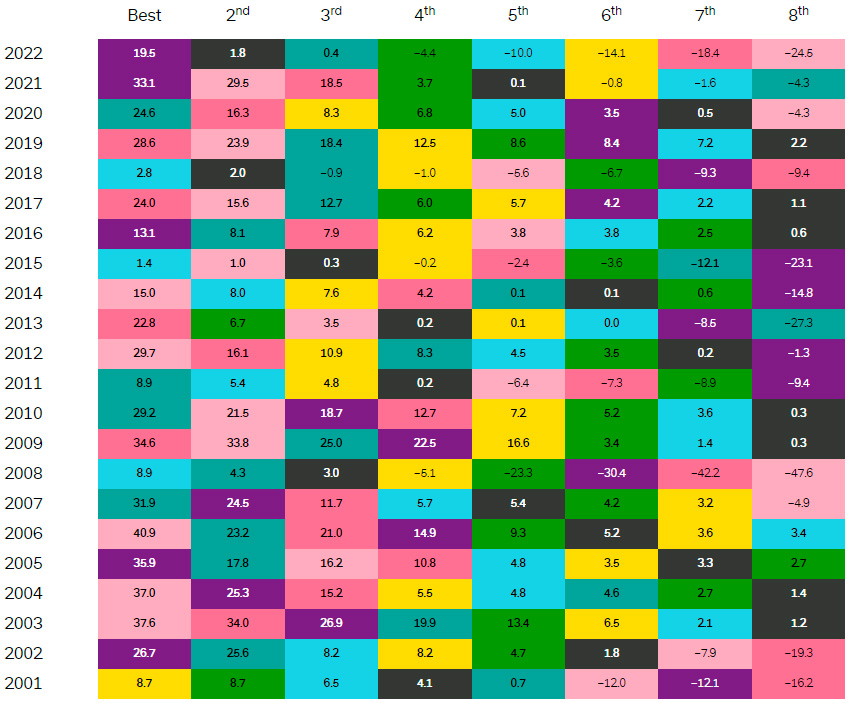

Performance of a balanced portfolio since 1900

A balanced portfolio is positive in 97% of cases in any 5-year period over 122 years.

Looking at the big picture:

Source: Vontobel 2022, Bloomberg, Global Financial Data; income from the S&P 500 Index and US Government Bonds from 1900 to end of 2022, annual total returns (including dividends), gross. Note: Historical data doesn’t guarantee the same course of events in the future. Not applicable to all regions and/or investment styles.

A balanced portfolio can be exemplified by 45% equities and 55% government bonds. A holding period of five years and more is the kind of long-term perspective investors favor.

Now let’s do the math: 97% of the time, a balanced portfolio spanning five years or more in any given timeframe ends up in positive territory and yielded, in fact, +7,3% per annum over the last 122 years.

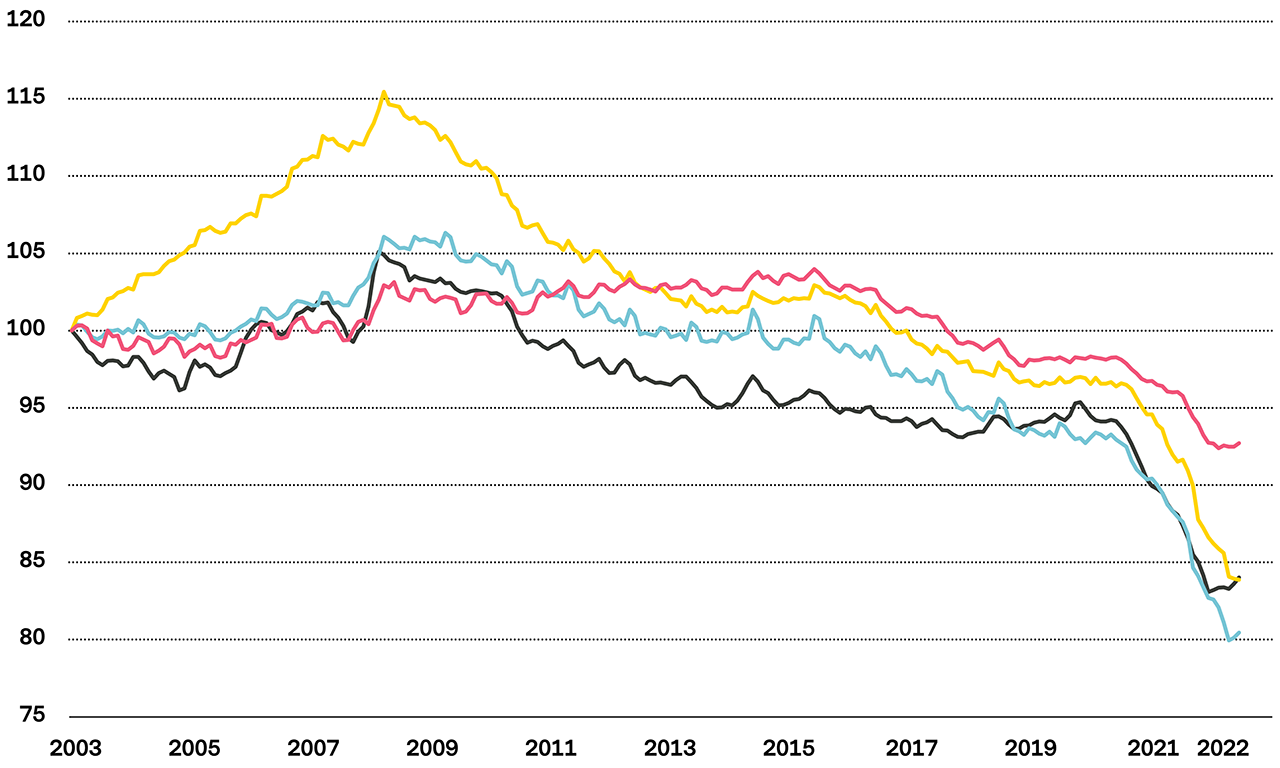

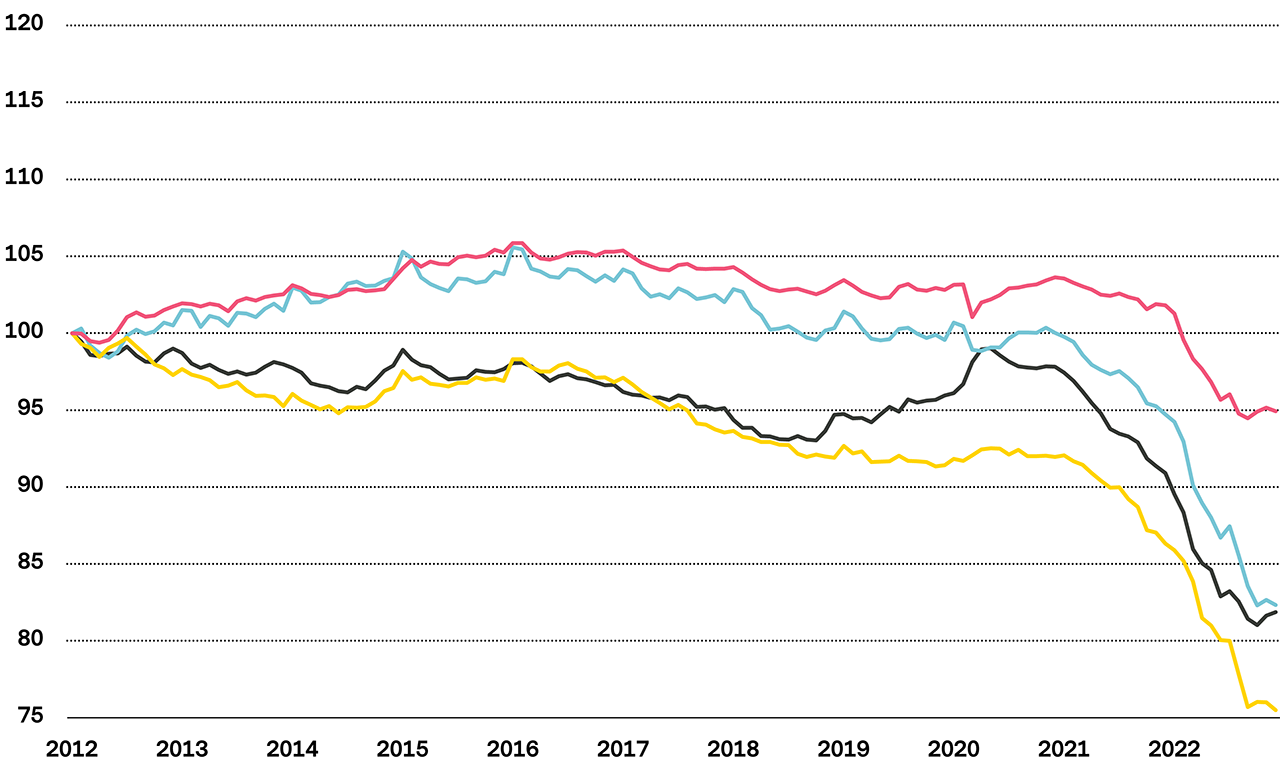

Myth 5: Passive is always the best way to go

Net returns of an actively managed fund vs. an index

Source: Bloomberg, net returns of the Vontobel Fund mtx Sustainable Emerging Markets Leaders A (VGREMEI LX Equity) versus the MSCI Emerging Markets index (MXEF) from 16.07.2011, when the fund was launched, to 31.12.2021.

Note: Not all actively managed funds succeed in beating a comparable, index-based passive product. According to Morningstar’s European Active/Passive Barometer 2021, active funds’ success rates over the ten years through June 2021, were less than 25% in nearly two-thirds of the categories surveyed. Past performance is not a reliable indicator of current or future performance. Performance data does not take into account any commissions and costs charged when shares of the fund are issued and redeemed, if applicable. The return of the fund may go down as well as up due to changes in rates of exchange between currencies

Published on 21.05.2022 CEST