Pillar 3a: actively managed for attractive retirement planning

It’s well known that simply building wealth is not enough. Ideally, it should be protected against inflation and, if possible, increased. One way to achieve this is by investing capital in securities. Given the often large amounts of capital that accumulate in pillar 3a accounts over the years, it makes sense to apply this principle to retirement provisions as well.

Why choosing a securities solution pays off in the long run

Which option offers the better potential returns? A security-oriented fixed interest account or a market-linked investment in securities?

Here’s a sample calculation using our app-based investment solution, Volt 3a:

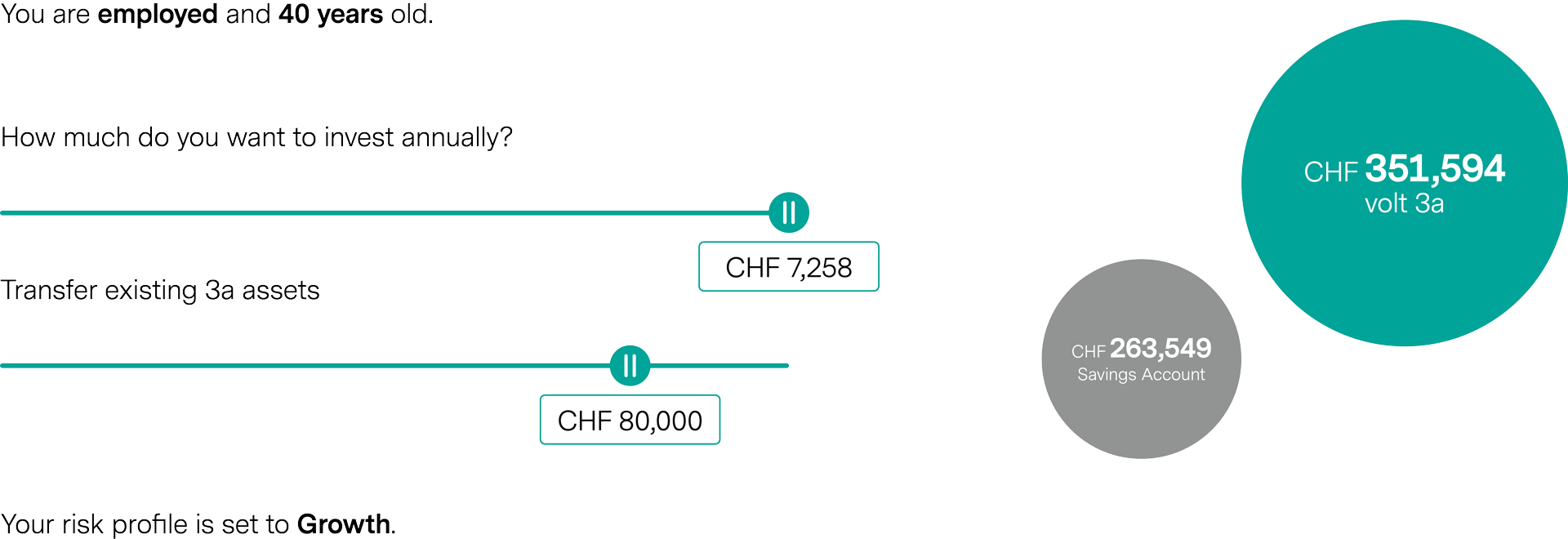

Assuming a remaining working period of 25 years, an initial capital of CHF 80,000 in your pillar 3a account, and an annual contribution of CHF 7,258.

According to the Volt 3a calculation model, a 3a securities portfolio with a “growth” investment strategy would reach an expected final asset value of around CHF 352,000. In comparison: in the same period, a savings account would yield around CHF 264,000.

Regularly investing your savings capital according to your personal investment strategy is therefore a key success factor in retirement savings.

Published on 10.06.2025 CEST

ABOUT THE AUTHORS

Show more articles

Show more articlesMichael Eugster

Senior Financial Planner

Show more articles

Show more articlesClaude Frosio

Head Tax Consulting