Investment risks1

A company's stock price may be adversely affected by changes in the company, its industry or economic environment and prices can change quickly. Equities typically involve higher risks than bonds and money market instruments.

The sub-fund’s investments may be subject to sustainability risks. The sustainability risks that the sub-fund may be subject to are likely to have an immaterial impact on the value of the sub-fund’s investments in the medium to long term due to the mitigating nature of the sub-fund’s ESG approach. The sub-fund’s performance may be positively or negatively affected by its sustainability strategy. The ability to meet social or environmental objectives might be affected by incomplete or inaccurate data from third-party providers. Information on how environmental and social objectives are achieved and how sustainability risks are managed in this sub-fund may be obtained from vontobel.com/sfdr.

1 The listed risks concern the current investment strategy of the fund and not necessarily the current Portfolio. Subject to change, without notice, only the current prospectus or comparable document of the fund is legally binding.

Important legal information

This document is for information purposes only and does not constitute an offer, solicitation or recommendation to buy or sell shares of the fund/fund units or any investment instruments, to effect any transactions or to conclude any legal act of any kind whatsoever. Subscriptions of shares of the fund should in any event be made solely on the basis of the fund’s current sales prospectus (the “Sales Prospectus”), the Key (Investor) Information Document (“K(I)ID”), its articles of incorporation and the most recent annual and semi-annual report of the fund and after seeking the advice of an independent finance, legal, accounting and tax specialist. This document is directed only at recipients who are institutional clients, such as eligible counterparties or professional clients as defined by the Markets in Financial Instruments Directive 2014/65/EC (“MiFID”) or similar regulations in other jurisdictions, or as qualified investors as defined by Switzerland’s Collective Investment Schemes Act (“CISA”).

Neither the fund, nor the Management Company nor the Investment Manager make any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of an assessment of ESG research and the correct execution of the ESG strategy. As investors may have different views regarding what constitutes sustainable investing or a sustainable investment, the fund may invest in issuers that do not reflect the beliefs and values of any specific investor.

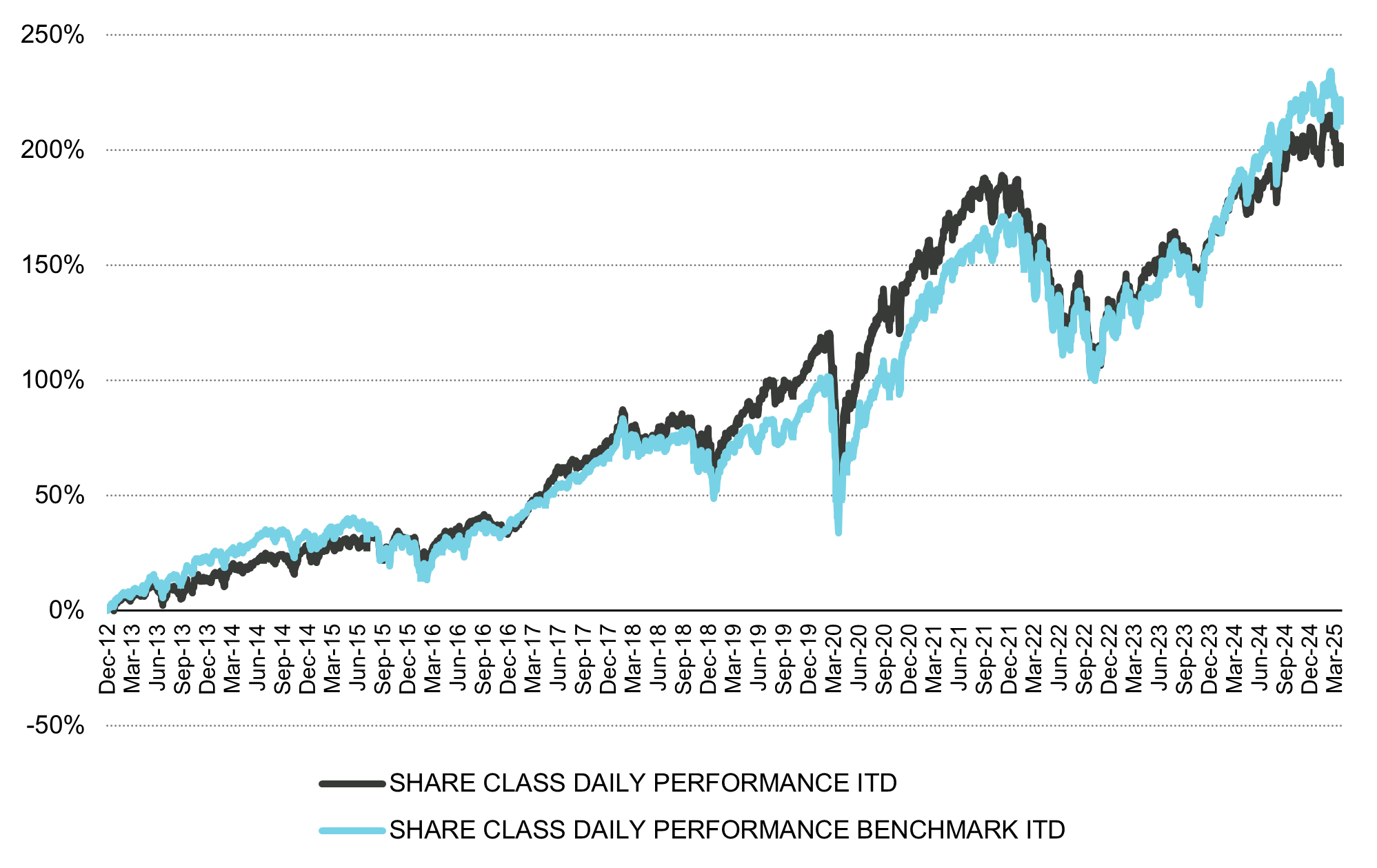

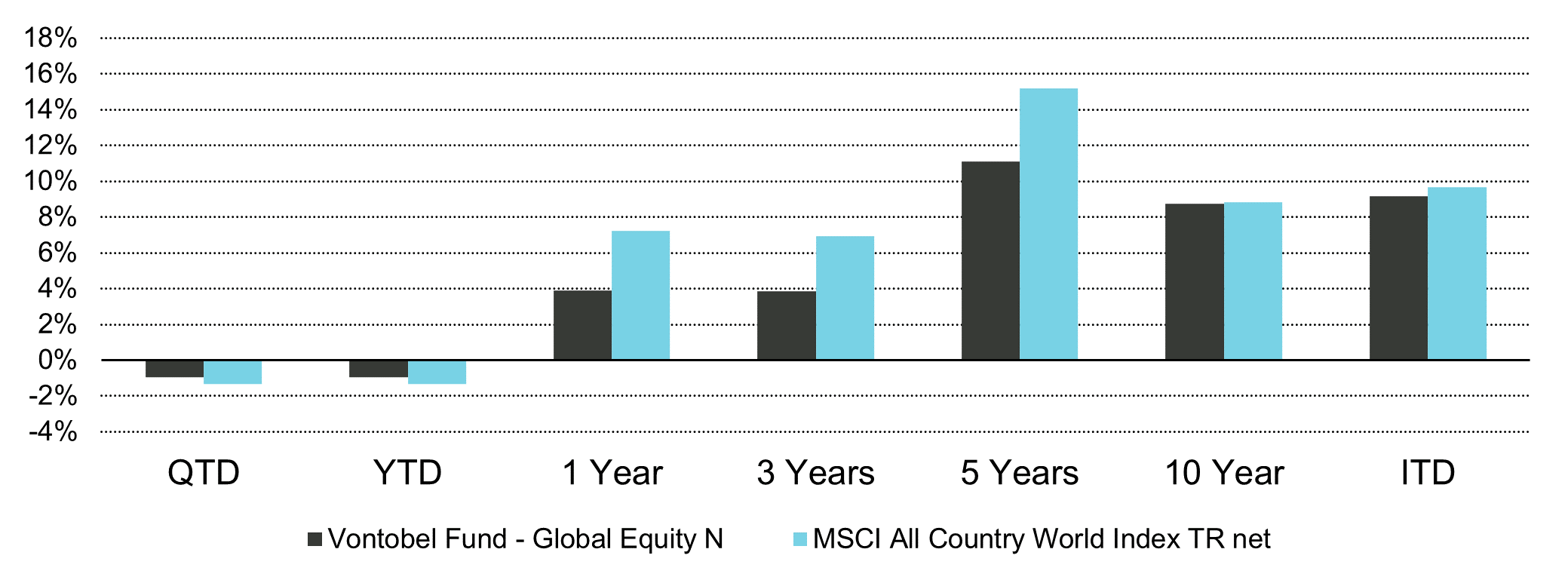

Past performance is not a reliable indicator of current or future performance.

Performance data does not take into account any commissions and costs charged when shares of the fund are issued and redeemed, if applicable. The return of the fund may go down as well as up, e.g. due to changes in rates of exchange between currencies. The value of the money invested in the fund can increase or decrease and there is no guarantee that all or part of your invested capital can be redeemed.

Interested parties may obtain the above-mentioned documents free of charge from the authorized distribution agencies and from the offices of the fund at 49 Avenue J.F. Kennedy, L-1855 Luxembourg, the facilities agent in Austria: Erste Bank der oesterreichischen Sparkassen AG, Am Belvedere 1, A-1100 Vienna, the representative in Switzerland: Vontobel Fonds Services AG, Gotthardstrasse 43, 8022 Zurich, the paying agent in Switzerland: Bank Vontobel AG, Gotthardstrasse 43, 8022 Zurich, the European facilities agent for Germany: PwC Société coopérative - GFD, 2, Rue Gerhard Mercator B.P. 1443, L-1014 Luxembourg, Email: lu_pwc.gfd.facsvs@pwc.com, gfdplatform.pwc.lu/facilities-agent/, the information agent in Liechtenstein: LLB Fund Services AG, Äulestrasse 80, FL-9490 Vaduz. Refer for more information on the fund to the latest prospectus, annual and semi-annual reports as well as the key (investor) information documents (“K(I)ID”). These documents may also be downloaded from our website at vontobel.com/am. A summary of investor rights (including information on representative actions for the protection of the collective interests of consumers under EU Directive 2020/1828) is available in English under: vontobel.com/vamsa-investor-information. Vontobel may decide to terminate the arrangements made for the purpose of marketing its collective investment schemes in accordance with Article 93a of Directive 2009/65/EC. Denmark: The KID is available in Danish. Finland: The KID is available in Finnish. The KID is available in French. The fund is authorized to the commercialization in France. Refer for more information on the funds to the KID. Italy: Refer for more information regarding subscriptions in Italy to the Modulo di Sottoscrizione. For any further information: Vontobel Asset Management S.A., Milan Branch, Piazza degli Affari 2, 20123 Milano, telefono: 0263673444, e-mail: clientrelation.it@vontobel.com. Netherlands: The Fund and its sub-funds are included in the register of Netherland's Authority for the Financial Markets as mentioned in article 1:107 of the Financial Markets Supervision Act (“Wet op het financiële toezicht”). Norway: The KID is available in Norwegian. Please note that certain sub-funds are exclusively available to qualified investors in Andorra or Portugal. In Spain, funds authorized for distribution are recorded in the register of foreign collective investment companies maintained by the Spanish CNMV (under number 280). The KID can be obtained in Spanish from Vontobel Asset Management S.A., Sucursal en España, Paseo de la Castel-lana, 91, Planta 5, 28046 Madrid. Sweden: The KID is available in Swedish. The fund and its sub-funds are not available to retail investors in Singapore. Selected sub-funds of the fund are currently recognized as restricted schemes by the Monetary Authority of Singapore. These sub-funds may only be offered to certain prescribed persons on certain conditions as provided in the “Securities and Futures Act”, Chapter 289 of Singapore. This document was approved by Vontobel Pte. Ltd., which is licensed with the Monetary Authority of Singapore as a Capital Markets Services Licensee and Exempt Financial Adviser and has its registered office at 8 Marina Boulevard, Marina Bay Financial Centre (Tower 1), Level 04-03, Singapore 018981. This advertisement has not been reviewed by the Monetary Authority of Singapore. The fund is not authorized by the Securities and Futures Commission in Hong Kong. It may only be offered to those investors qualifying as professional investors under the Securities and Futures Ordinance. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution and if you are in doubt about any of the contents of this document, you should obtain independent professional advice. This document was approved by Vontobel (Hong Kong) Ltd., which is licensed by the Securities and Futures Commission of Hong Kong and provides services only to professional investors as defined under the Securities and Futures Ordinance (Cap. 571) of Hong Kong and has its registered office at 1901 Gloucester Tower, The Landmark 15 Queen’s Road Central, Hong Kong. This advertisement has not been reviewed by the Securities and Futures Commission.The fund authorised for distribution in the United Kingdom and entered into the UK’s temporary marketing permissions regime can be viewed in the FCA register under the Scheme Reference Number 466625. The fund is authorised as a UCITS scheme (or is a sub fund of a UCITS scheme) in a European Economic Area (EEA) country, and the scheme is expected to remain authorised as a UCITS while it is in the temporary marketing permissions regime. This information was approved by Vontobel Asset Management S.A., London Branch, which has its regis-tered office at 3rd Floor, 70 Conduit Street, London W1S 2GF and is authorized by the Commission de Surveillance du Secteur Financier (CSSF) and subject to limited regulation by the Financial Conduct Authority (FCA). Details about the extent of regulation by the FCA are available from Vontobel Asset Management S.A., London Branch, on request. The KIID can be obtained in English from Vontobel Asset Management S.A., London Branch, 3rd Floor, 70 Conduit Street, London W1S 2GF or downloaded from our website vontobel.com/am.

This document is not the result of a financial analysis and therefore the “Directives on the Independence of Financial Research” of the Swiss Bankers Association are not applicable. Vontobel and/or its board of directors, executive management and employees may have or have had interests or positions in, or traded or acted as market maker in relevant securities. Furthermore, such entities or persons may have executed transactions for clients in these instru-ments or may provide or have provided corporate finance or other services to relevant companies.

The MSCI data is for internal use only and may not be redistributed or used in connection with creating or offering any securities, financial products or indices. Neither MSCI nor any other third party involved in or related to compiling, computing or creating the MSCI data (the “MSCI Parties”) makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and the MSCI Parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to such data. Without limiting any of the foregoing, in no event shall any of the MSCI Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

Although Vontobel believes that the information provided in this document is based on reliable sources, it cannot assume responsibility for the quality, correctness, timeliness or completeness of the information contained in this document. Except as permitted under applicable copyright laws, none of this information may be reproduced, adapted, uploaded to a third party, linked to, framed, performed in public, distributed or transmitted in any form by any pro-cess without the specific written consent of Vontobel. To the maximum extent permitted by law, Vontobel will not be liable in any way for any loss or damage suffered by you through use or access to this information, or Vontobel’s failure to provide this information. Our liability for negligence, breach of contract or contravention of any law as a result of our failure to provide this information or any part of it, or for any problems with this information, which cannot be lawfully excluded, is limited, at our option and to the maximum extent permitted by law, to resupplying this information or any part of it to you, or to paying for the resupply of this information or any part of it to you. Neither this document nor any copy of it may be distributed in any jurisdiction where its distribution may be restricted by law. Persons who receive this document should make themselves aware of and adhere to any such restrictions. In particular, this docu-ment must not be distributed or handed over to US persons and must not be distributed in the USA.

Vontobel

Gotthardstrasse 43, 8022 Zurich

Telefon +41 58 283 71 50

Telefax +41 58 283 71 51

vontobel.com/am