Real estate gains tax in the event of a sale: rules and exceptions

Example 2: The long-term perspective

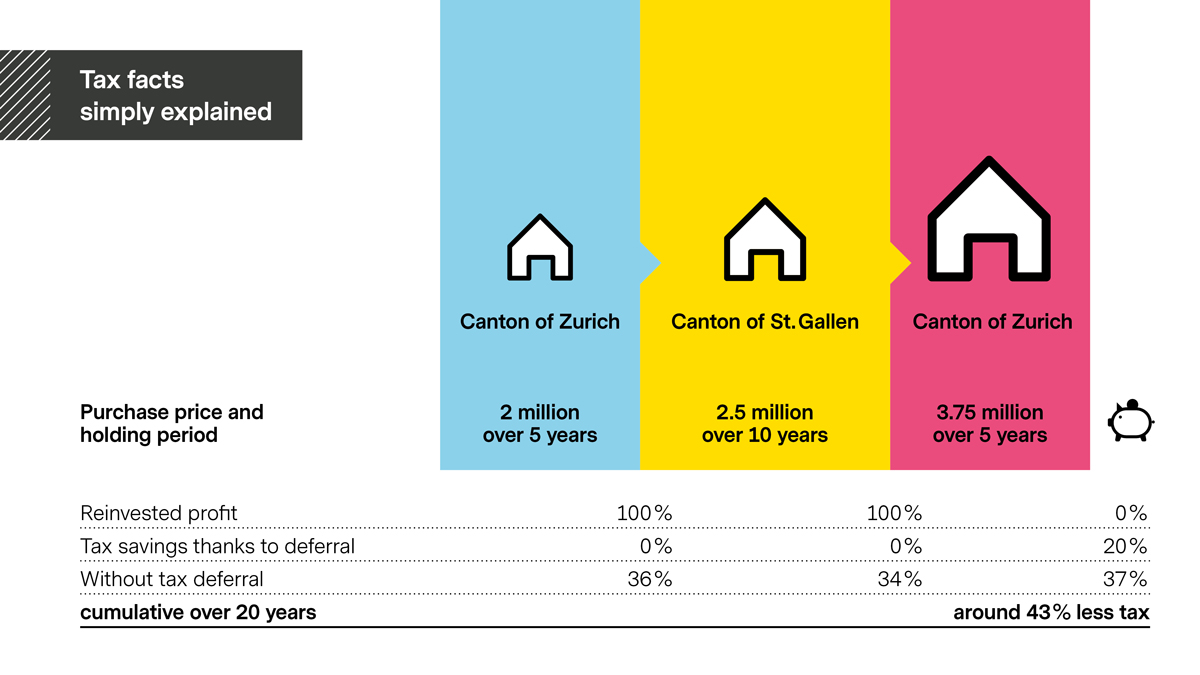

Real estate gains tax after 20 years of ownership and two moves

The first property in Zurich is sold after five years with a profit of CHF 500,000. The entire profit is reinvested in a replacement property in the canton of St. Gallen, allowing the deferral of the real estate gains tax. After ten years, this property is also sold. The profit of CHF 1.25 million is again fully reinvested in a replaced property in the canton of Zurich, allowing the deferral of the real estate gains tax a second time. After a total holding period of 20 years, the final sale takes place for CHF 4.5 million without any further reinvestment in an owner-occupied property within Switzerland. This results in a cumulative profit of CHF 2.5 million during the whole period. Thanks to the ability to defer the real estate gains taxes twice, a tax saving of approximately 43% or CHF 378,910 is achieved over 20 years.

Assumption: All three properties were owner-occupied throughout the entire holding period. All figures exclude property transfer tax.