Dividenden neu entdecken

Ergänzen Sie Ihre Einnahmen um planbare Dividendenzahlungen

What exactly is a dividend—and what should investors look out for?

A dividend is broadly speaking the cash distribution of some or all of a company’s profit to its shareholders. In uncertain times, when capital gains are low or even turning into losses, this payout can be a valuable source of income for investors.

Learn in this article how to judge the merits of dividends by understanding how companies decide to distribute dividends.

In this video: Follow the performance analysis of dividend stocks by JP Britz and Vadim Safranov, Portfolio Manager in Asset Management and Senior Client Portfolio Manager in Wealth Management. © Video: Vontobel 2022.

Most investors welcome dividends. Even the founder, CEO, and Chairman of a Swiss biotech company who for years advocated reinvesting every penny made back into his company, once told us that he was thrilled when he received the first dividend payment from his company—it gave him a feeling of satisfaction. For individual investors, receiving dividends is often a welcome cash inflow. In the case of institutional investors, such as insurance companies or pension funds, it helps them fund ongoing expenses.

Generally speaking, investors and companies attach considerable importance to dividends. In the US, “Dividend Aristocrats” constitute a stock market index of companies in the S&P 500 that have paid and increased their base dividend in each of the past 25 consecutive years. On the downside, however, an unexpected cut in the dividend of a “dividend” stock (high, reliable dividend payment) often leads to a very negative share price reaction as it is considered by investors to be a major negative signal regarding the company’s long-term prospects.

Benefits of dividends

One of the long-term benefits associated with stocks that pay high dividends are potentially stronger returns and lower volatility—under certain circumstances, dividends may help cushion losses during bear markets. If we take the last three bear markets, when the S&P 500 declined over 30 percent, the “S&P 500 Dividend Aristocrats” outperformed the S&P 500 Index on two occasions. First, during the bursting of the tech bubble (September 2000 to October 2002) and then again during the Global Financial Crisis (October 2007 to March 2009). In both cases, the outperformance was significant or even very significant. More recently, during the COVID-19 sell-off, the “Dividend Aristocrats” marginally underperformed.

How to explain the different performance of dividend stocks?

The stellar outperformance during the bursting of the tech bubble should be not surprising. Technology companies are mostly growth companies: They reinvest their capital rather than distributing it to shareholders. Thus, the absence of technology stocks in the “Dividend Aristocrats” was the driver of the outperformance.

In turn, given that technology and growth stocks in general benefitted, at least to a certain degree, from some of the effects related to the COVID-19 pandemic, “Dividend Aristocrats” marginally underperformed. In light of the above, the question must be asked:

“Is the outperformance of the ‘S&P Dividend Aristocrats’ a function of the dividend, or rather the generally more defensive business model of its constituents, compared to a much higher share of growth companies in the S&P 500?”

| S&P 500 | S&P 500 DIVIDEND ARISTOCRATS | OUTPERFORMANCE | |

| Bursting of Tech Bubble (1.9.2000–9.10.2002) | –47.4% | +4.7% | +51.4% |

| Global Financial Crisis (9.10.2007–9.3.2009) | –55.2% | –47.2% | +8.0% |

| COVID-19 (19.2.2020–23.3.2020) | –33.8% | –35.2% | –1.4% |

Not all dividends are the same

Dividends cannot simply be taken at face value, as not all dividends are the same. Their future development, such as growth trajectory, stability, or predictability, depends on company-specific factors.

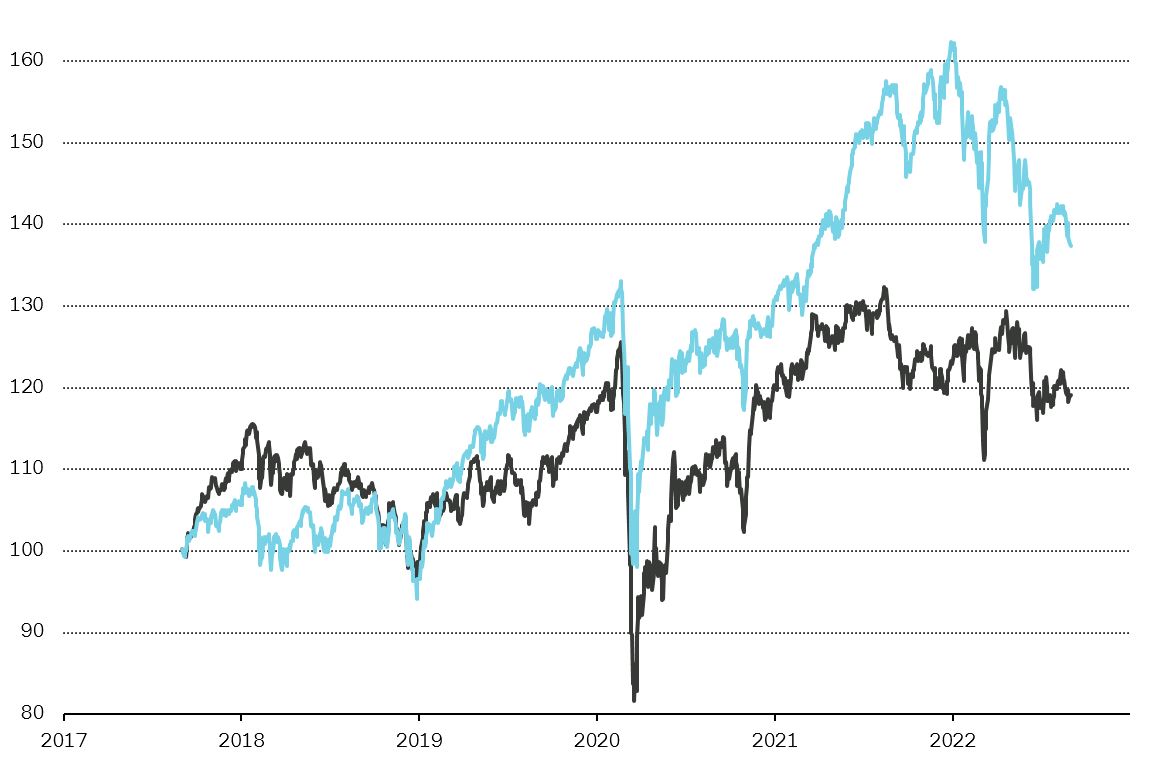

Investing in companies with the highest dividend yield risks falling short of a sound, long-term investment strategy. For illustrative purposes, we create an equal weighted portfolio over the last five years which includes the ten Swiss SPI stocks with the highest dividend yield at the time (we excluded micro-cap companies). Over this time horizon, the total shareholder return* of the portfolio underperformed the benchmark (SPI) even under the assumption of zero taxes on dividends and no transaction costs.

Consequently, investors should assess each company’s dividend prospects and diversify their investments. A high dividend yield can be the result of a company’s strong cash generation, a sign of distress, or a lack of growth opportunities.

Performance of the Swiss Performance Index (SPI) compared to a dividend portfolio

© Vontobel 2022

▬ Sample portfolio consisting of the ten highest dividend stocks at the time, equally weighted, in CHF

▬ Swiss Performance Index (SPI) in CHF

Data spanning a five-year period from 31.08.2017 to 31.08.2022. Dividend stocks limited to companies with a market capitalization of at least 500 million Swiss francs.

Note: Historical data doesn’t guarantee the same course of events in the future. Not applicable to all regions and/or investment styles.

How are dividends taxed in Switzerland?

In Switzerland, dividends are taxed at the personal income tax rate. Therefore, investors should take a holistic view of their financial situation before tapping the potential of dividend stocks.

What are dividends with tax privileges?

Or contact our Wealth Planning team to learn more

Dividend payouts from a company perspective

Capital allocation is one of the most critical means of putting a company’s strategy into action. A core part of capital allocation is a company’s capital return policy, provided it has capital it can, and wants, to return to shareholders. Over the long term, a company can allocate capital either from internal sources (cash flow, including selling assets) or access external sources (banks or capital markets).

- Capital is allocated to running as well as growing the company, both organically and by means of acquisitions.

- Beyond satisfying these purposes, the company can return excess cash to shareholders either through dividends or other methods, such as share buybacks.

The proportion of internally generated funds a company allocates to which end depends on its strategy and the environment in which it operates. If a company has many high-return, strategic growth projects, it is likely to allocate most or all of its capital to these projects to generate future value for its share- and stakeholders. Two examples:

Dividend-paying company |

Low-dividend-paying company |

| Nestlé is an example of a company with a clearly defined capital allocation strategy* based on clearly defined priorities: | Logitech, for instance, is a different case. The company is a growth stock not a dividend stock. Accordingly, it has different capital allocation priorities: |

|

|

| With respect to the dividend itself, the company targets an increasing dividend in absolute terms, i.e., in Swiss francs. From a research viewpoint, we believe this is perfectly sensible based on the company’s cash generating capacity and visibility. Given Nestlé’s substantial cash generation and its global position, paying a dividend has a very high priority. | Consequently, Logitech allocates a far smaller proportion of its cash flow to dividends. As a result, it doesn’t attract investors who focus heavily on regular dividend income. |

* As disclosed on Nestlé’s official website.

** As disclosed on Logitech’s official website: latest dividend report and share repurchase history.

Disclaimer: This comparison should not be construed as an investment recommendation or rating. The companies mentioned in this paper are only used as examples to illustrate the principle.

Conclusion

Companies with strong dividends tend to outperform in uncertain times. However, there is no guarantee of that, especially as uncertainty can be attributable to many different reasons and will not necessarily lead to a bear market. In the last 20 years, bear markets have been a stronger predictor of dividend stocks outperforming. The exception was the very short, violent bear market triggered by the COVID-19 pandemic in early 2020, which was not a “typical” bear market.

Most importantly, in our view, investors looking for dividends need to understand companies’ business models and their capital allocation policies in order to assess their future potential and how reliable they may be. This should help them tailor their selection to their specific financial needs and goals.

Publiziert am 12.09.2022 MESZ